For the past decade, blockchain has been viewed by many in the Banking, Financial Services, and Insurance (BFSI) sector as a solution in search of a problem. However, as we navigate through late 2025 and into 2026, the narrative has shifted decisively. Leading institutions like JPMorgan, HSBC, Citi, and BlackRock are pioneering use cases in payments, asset tokenization, and trade finance.

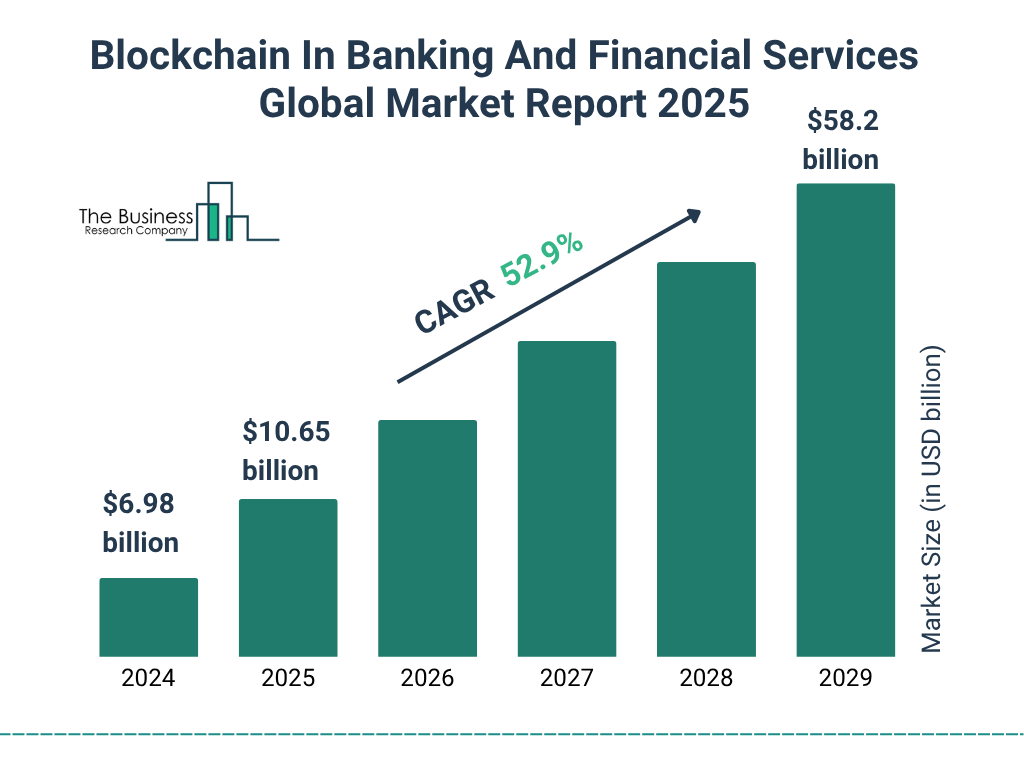

The global market for blockchain in banking and financial services, valued at approximately $6.98 billion in 2024, is projected to expand at a CAGR of 52.9%, reaching nearly $58.2 billion by 2029.

In the insurance sector, the growth curve is even steeper, with projections vaulting from $4.06 billion in 2024 to nearly $98 billion by 2035.

We are now in the era of industrialization, and the question is how the underlying rails of finance, settlement, custody, clearing, and payment will be rebuilt to accommodate the demand for 24/7 liquidity, atomic settlement, and programmable capital. With regulatory frameworks such as MiCA and the GENIUS Act now in force, blockchain has unprecedented opportunities for revenue growth, operational efficiency, and competitive differentiation in the BFSI sector, which could create a perfect storm for another round of institutional adoption.

Banking Sector Pain Points and Blockchain

The Blockchain Pulse Survey 2025, conducted by PwC and others on Swiss Banks, identifies the motivations for their adoption of blockchain. Although this data was collected for Switzerland, these factors apply to players globally.

Modern banking infrastructure confronts five systemic bottlenecks that blockchain directly addresses:

- Traditional correspondent banking routes international transfers through 3-5 intermediaries, resulting in 3-5-day settlement times and costs of 2-7% due to combined fees, foreign exchange spreads, and intermediary charges. Manual reconciliation processes compound delays and expose institutions to settlement risk. Banks traditionally maintain nostro/vostro accounts with billions in prefunded balances across correspondent banks to facilitate payment flows.

- 77% of banks report analyst shortages in anti-money laundering monitoring, as per the Hawk study, while 40% report high false-positive rates in transaction screening. High transaction volumes overwhelm outdated systems and create compliance risks and staffing burnout. Legacy infrastructure produces data validation errors that trigger regulatory fines.

- Industry-wide fraud averaged 0.8 basis points in 2024, with unauthorized account takeover schemes comprising 71% of incidents. Large institutions faced 4× higher losses than smaller banks, as sophisticated AI-driven attacks exploit legacy security gaps.

- Batch-processing cycles for securities settlement (T+1 in the U.S. since 2024) create credit and liquidity risks for high-volume institutions. Poor data integration across custodians and counterparties necessitates manual reconciliation, delaying capital availability and increasing operational costs.

- The Hawk study says 30% of banks identify outdated technology as their primary AML bottleneck. Siloed databases hinder loan reviews, contract audits, risk modeling, and regulatory reporting automation. This forces manual workarounds that slow operations and increase error rates.

Distributed ledger and tokenization architectures directly remediate these pain points

1. Real-Time Settlement Infrastructure:

Blockchain-based payment networks enable 24/7 atomic settlement in minutes versus days using traditional banking channels. This reduces liquidity buffers, eliminates float requirements, freeing capital for productive deployment.

Tokenized deposit systems provide programmable money with delivery-versus-payment (DvP) finality, which eliminates settlement risk as securities transfer and cash payment occur simultaneously and atomically. Either both legs settle or neither does. This contrasts with legacy systems, where securities might move before payment confirmation, which creates principal risk.

DTCC could be the biggest example here. They received authorization on December 11, 2025, to tokenize DTC-custodied assets, including Russell 1000 securities, ETFs, and U.S. Treasuries, using blockchain.

2. Stablecoins are one of the biggest enablers for global payments

While stablecoins are often associated with retail usage and remittances and were mostly restricted to crypto natives before, a growing share of volume is being driven by business-to-business (B2B) transactions like cross-border payments, supplier settlements, invoicing, vendor payments, treasury operations, and other enterprise use cases. Over $6.0 billion by mid-2025 was just B2B volume.

Get in Touch with Our Experts to Build, Deploy, and Scale with Confidence — Get started with Zeeve Today

.

This removes the cross-border costs significantly, along with fewer intermediaries and faster settlements. It’s no wonder that US Treasury Secretary Scott Bessent has said, “We are going to keep the U.S. the dominant reserve currency in the world, and we will use stablecoins to do that.”

The growth projection is huge. Coinbase expects it to grow to 1.2T while the US Treasury Borrowing Advisory Committee estimates it could be 2T by 2028.

3. Immutable Identity and Compliance:

Shared KYC ledgers enable reusable digital identities that are verified once and trusted across institutions, which reduces onboarding friction. Smart contracts automate transaction monitoring against evolving AML regulations, while transparent audit trails reduce false-positive rates. Fraud detection improves through pattern recognition across tamper-proof transaction histories and cryptographic verification of sender/receiver identities.

The SWIFT proposed blockchain ledger that will include 30+ major financial institutions globally could be the most recent example that endorses this capability for scale.

4. Network Decentralization

Distributed architecture eliminates single points of failure, enables continuous operation outside business hours, and automates rule enforcement through protocol-level smart contracts, which reduces reliance on manual compliance teams. Point-to-point data sharing can ensure that only relevant parties access sensitive KYC information, and a custom blockchain ensures controlled validator participation for regulatory compliance. The use of smart contracts can be highly customized to meet complex business logic. For example,

- Funds are released only upon delivery confirmation, regulatory approval, or multi-party signatures.

- Smart contracts match payments to invoices, eliminating manual matching processes.

- Credit lines activate automatically when balance thresholds are breached etc.

Financial Services Industry and Where Blockchain Fits?

The broader financial services sector, which encompasses asset management, securities settlement, trade finance, and custody, has distinct operational and market frictions:

- The asset management industry has a profitability pressure. The Global assets under management reached $147 trillion by June 2025, yet profitability remains constrained by rising costs.

As per this 2025 McKinsey Asset Management report, asset managers continue to operate on aging infrastructure that is expensive to maintain, which made the operating expenses surge 7% to $167 billion in 2024, driven by technology investments (+9%), product complexity (+8%), and distribution expenses (+8%).

Multi-asset portfolio expansion increased specialized headcount by 60% for product specialists and 30% for operations teams from 2020 to 2024, compressing margins. Private markets fundraising declined from a $1.7 trillion peak to $1.1 trillion in 2024, with muted exits in private equity and real estate creating liquidity constraints.

- Settlement failures expose counterparties to credit and liquidity risks, triggering penalties under the EU’s Settlement Discipline Regime (0.5-1 basis point fines). The shift to T+1 settlement cycles in the U.S., Canada, and India increased risk of failure by compressing time for inventory sourcing and error resolution. Lack of lifecycle transparency across custodians hinders proactive fail prevention.

- International trade financing entails layered risks: product performance warranties, transport hazards (90% by sea freight), currency-exchange rate exposure, and fraud/documentary verification across borders. Traditional processes require manual coordination among exporters, importers, insurers, and banks, creating delays and increasing dispute-resolution costs.

- T+1 settlement heightened custody challenges for securities lending for share recalls and inventory management. Legacy batch processing increases fail rates, while real-time data gaps between custodians and lenders impair collateral optimization.

As per KPMG, even moving to a T+0 day is a very soon possible alternative, leveraging blockchain.

Blockchain-Driven Transformation in Financial Services Industry

Tokenized Assets and RWA Platforms:

Asset tokenization converts traditional securities like equities, bonds, funds, and real estate into blockchain-native tokens with programmable attributes. This enables:

- Fractional Ownership: Lower investment minimums democratize access to institutional-grade assets. Conventional securities impose minimum investment thresholds. Real estate funds: $25,000-100,000 minimums for institutional REITs

Private equity: $250,000+ accredited investor requirements.

Smart contracts enable fractional token issuance, which can give proportional ownership.

Apart from these, 24/7 Trading, Instant Settlement, Transparent Custody, immutable on-chain records, and Automated Compliance are some of the common benefits we have discussed in banking as well.

The pie chart below shows the total value of real-world assets distribution on-chain

By December 2025, $18.81 billion in real-world assets had been tokenized on public blockchains, with Ethereum accounting for $12.4 billion (66% share) and Solana ranking third at $800 million.

For equity markets, there are also tremendous possibilities. Here’s a quote from the Silicon Valley Bank finance outlook for 2026:

Tokenized U.S. Treasuries Explosion

Tokenized U.S. Treasuries are the single largest RWA category, which accounts for over half of total non-stablecoin tokenized assets. This became so popular because of 4 primary reasons:

- Low-risk profile: AAA sovereign credit quality attracts conservative institutional capital

- Regulatory clarity: U.S. Treasury securities have well-established legal frameworks

- Yield competitiveness: 4-5% APY versus near-zero traditional bank deposits

- Liquidity: Deep underlying Treasury markets enable large-scale tokenization

Tokenized Treasury products grew > 200% year-over-year from $3 billion (Early 2025) to $8.7 billion (December 2025), with 62 live products across eight major chains. These funds provide a 4-5% programmable yield for institutional cash management with on-chain liquidity and real-time settlement.

And the use case and target segment for each of these are different. For example, Circle USYC (USD Yield Coin) is for non-U.S. institutional investors where direct U.S. Treasury access is restricted. The main use cases are:

- Asian institutional cash: Singapore/Hong Kong funds park dollars with yield versus non-interest USDC

- Cross-border settlement: Use USYC for international trade finance with embedded yield during float

- Regulatory arbitrage: Access U.S. Treasury yields without direct U.S. broker-dealer relationships

Another example could be Franklin Templeton BENJI, which is an OnChain U.S. Government Money Fund that has around 945 mixed retail/institutional holders. This fund gave Retail accessibility. It has Lower minimums than traditional Franklin funds ($1M+ typical).

So the use cases are varied, and the potential is huge in the coming months.

Smart Contracts for Trade Finance

International trade financing involves $15-20 trillion annual flows across complex multi-party processes where multiple layers of workflow inefficiencies exist for Letter of Credit (LC) Issuance, Document Handling, Payment Release, Dispute Resolution, and Fraud Risks.

Blockchain-based trade platforms automate the release of payments, warranty verification, and insurance claim triggers based on predefined milestones (e.g., delivery confirmation via IoT sensors). This mitigates fraud and documentary risks through verifiable on-chain proofs, thereby reducing dispute-resolution timelines.

Insurance Sector Pain Points and Blockchain

The insurance sector faces distinct operational and customer experience challenges that blockchain architectures specifically address:

- Traditional claims workflows involve multiple departmental touchpoints, such as underwriting, adjusters, reinsurers, and payment processors. These create fragmentation for both employees and customers. Manual verification and approval steps extend settlement timelines from weeks to months, particularly for complex workers’ compensation, health, and business insurance claims.

- According to CoinLaw’s “Insurance Fraud Statistics 2025, Insurance fraud exceeds $80 billion annually worldwide. Identity theft cases increased by 49% through 2025, with synthetic identity schemes causing $47 billion in losses in 2024. Fraudulent claims, duplicate submissions, exaggerated damages, and fabricated incidents strain investigative resources.

- Sensitive customer health, financial, and personal information requires robust encryption and audit trails. Data breaches expose insurers to regulatory penalties and reputational damage, necessitating tamper-proof record systems.

- While parametric insurance (automatic payouts triggered by objective events like weather data) offers operational advantages, adoption faces four obstacles:

- Basis Risk: Payouts may not match actual policyholder losses if triggers imperfectly correlate with damages

- Consumer Awareness: Limited understanding of parametric mechanisms versus traditional indemnity models

- Distribution Costs: High customer acquisition expenses for niche products

- Data Reliability: Dependence on accurate, tamper-proof trigger data (weather sensors, satellite imagery)

- Multi-party reinsurance contracts require extensive data exchange between primary insurers, reinsurers, and brokers. Manual reconciliation of premiums, claims, and reserves creates delays and operational costs estimated at $5-10 billion industry-wide, as per EY.

Blockchain Insurance Solutions

The impact of addressing these challenges on the CAGR is significant.

Smart Contract Claims Automation

Blockchain-based policies encode claims criteria as executable code. When predefined triggers occur (as verified by oracles), smart contracts automatically release payouts without manual adjuster intervention, reducing settlement time from months to days. Immutable records prevent duplicate or fraudulent claims.

Decentralized Identity (DID) for Underwriting

Shared blockchain identity systems enable:

- KYC Efficiency: Verify customer data once, reuse across insurers

- Fraud Prevention: Detect synthetic identities through cross-referenced on-chain histories

- Risk Assessment: Access comprehensive policyholder data from tamper-proof sources

Parametric Oracles for Instant Payouts

Integration with Oracle networks (e.g., Chainlink) enables smart contracts to ingest real-world data—weather stations, flight trackers, and seismic sensors—and execute automatic payouts when thresholds are met. This minimizes basis risk through precise trigger calibration and eliminates claims processing overhead.

Reinsurance Shared Ledgers

Distributed ledgers provide real-time data synchronization across insurers, reinsurers, and regulators. Single-source-of-truth architecture cuts reconciliation cycles from quarterly to continuous, reducing operational costs and improving capital efficiency.

Zeeve for BFSI Implementations

Zeeve is an enterprise-grade, neutral blockchain operating and enablement platform that helps organizations deploy, operate, and scale blockchain infrastructure with clear operational ownership.

For BFSI clients, compliance is non-negotiable and Zeeve is an ISO 27001, SOC 2 Type II, and GDPR compliant platform, ensuring that the infrastructure meets the stringent risk management standards required by global banks and insurers.

We follow a use-case-first approach and operate as a neutral orchestrator across competing blockchain stacks. Whether an institution chooses Hyperledger Besu or Enterprise Ethereum for a private inter-bank network or trade finance, or Avalanche L1s or ZKsync Prividium for a custom Layer 2 appchain, Zeeve’s platform supports them all.

Zeeve is trusted by 40+ enterprise clients, including Fortune 500 companies, across regulated and high-scale environments.

If you are in BFSI and want to integrate blockchain to your current stack, schedule a call with us to discuss how we could help.

{kind=link}